Amentum (AMTM): A Post-Spin Opportunity with Growth Potential

A resilient, undervalued business with critical government contracts and a $45B backlog poised for growth.

Introduction

Amentum (AMTM), a recent spin-off from Jacobs (J), offers investors a unique post-spin opportunity at an attractive valuation. Trading at 10x NTM P/E and delivering about a 10% free cash flow (FCF) yield based on company guidance, Amentum appears undervalued relative to its intrinsic strengths and competitive positioning. Despite its first earnings report as an independent public company showing no novel negative news, the stock sold off up to 12% today.

I believe this selloff reflects two primary factors:

Structural imbalances and mispricing often seen after spin-offs.

Concerns about potential spending constraints and efficiency initiatives under the new administration, primarily related to Department of Defense (DoD) budgets, which account for a significant portion of Amentum's revenue.

However, Amentum's record backlog and existing revenue composition offer resilience that investors may be underestimating. This resilience stems from the nature of Amentum's business:

Light on civilian-related workforce budgets

Involves critical missions such as environmental remediation

Important to national security

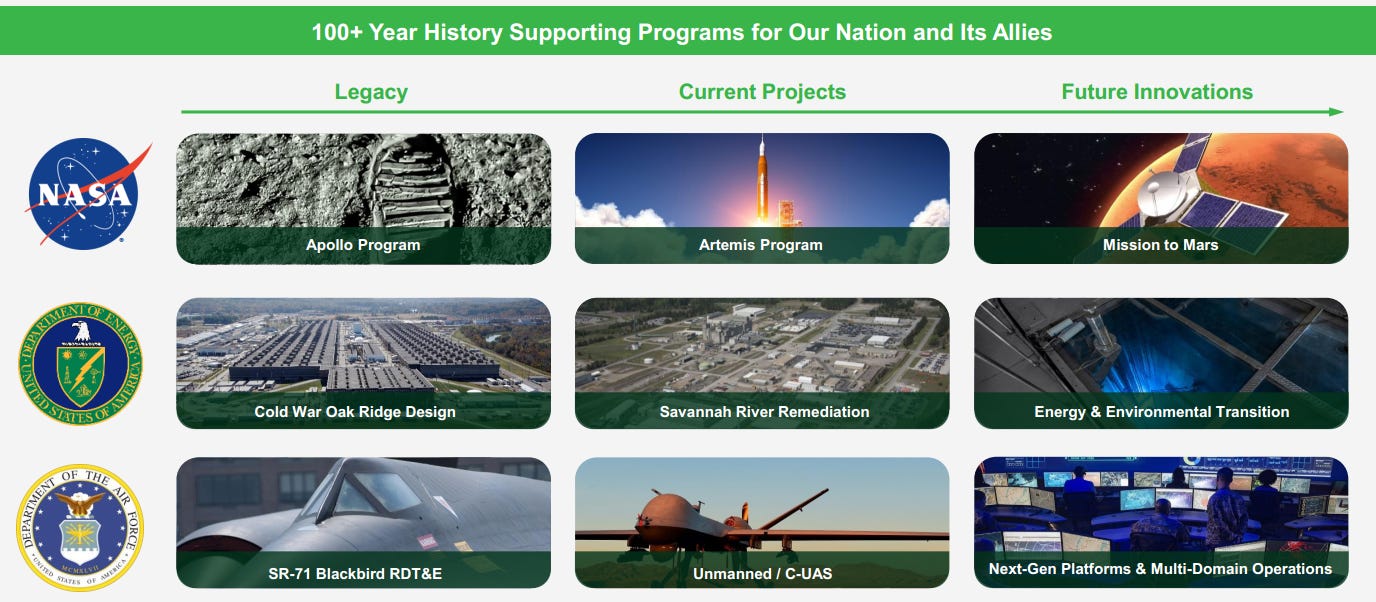

Furthermore, Amentum's multi-decade footprint working with major U.S. government agencies, spanning up to 70 years, reinforces its reputation and stability in executing critical government contracts.

1. Amentum: A Newly Independent Entity

Background of the Spin-Off

Amentum's spin-off from Jacobs earlier this year marked the creation of a leading advanced engineering and technology solutions provider with a $320 billion per year TAM. The rationale for the spin-off centered on unlocking value in Jacobs' Critical Mission Solutions (CMS) and Cyber & Intelligence businesses, enabling Amentum to focus on high-growth end markets in defense, technology, and sustainability.

As with many spin-offs, Amentum has faced:

Limited analyst coverage and investor visibility, leading to temporary mispricing.

Initial uncertainty around its financial and strategic guidance, further fueling investor hesitancy.

However, the company has now provided its first earnings report and guidance, delivering much-needed clarity for investors.

Market Reaction to the First Earnings Report

Key highlights from Amentum's inaugural earnings report include:

FY 2025 Revenue Guidance: $13.8B - $14.2B.

Adjusted EBITDA: $1.06B - $1.1B, signaling margin improvements.

Free Cash Flow: $475M - $525M, underlining robust cash generation potential.

Record Backlog: $45B, representing 3.2x revenue coverage and strong visibility into future revenue streams.

Despite these positive signals, the market reaction was severely negative after the conference call, with the stock declining up to 12%. This reaction likely reflects investor skittishness around broader industry concerns with upcoming initiatives from the new administration. However, no novel remarkable negative news was reported today, suggesting the selloff may be overdone.

Interestingly too, as I have posted on X recently, analyst estimates are far lower than I expect, or the company has guided the last several months at $1.41 per share for FY 2025. Granted, only two analyst provided estimates, and this bolsters the case for why spin-offs can provide attractive opportunities.

I had expected about $1.80 of EPS for 2025 and management came out with a $2.10 median guide yesterday evening. This guidance assumes no material impact on its operations due to changes from the new administration.